Introduction

Technically, you never need to buy any form of insurance to start or run a microgreen business. Is it a good idea to get insurance? Absolutely. States in the U.S. don’t require insurance to create an LLC or sole proprietorship. Banks don’t require insurance to open a bank account. This article will cover the various types of insurance for your microgreen business. It will detail their costs, when to buy each type, and who is likely to ask for proof of insurance.

General Liability Insurance

The first type of insurance you’ll want is commercial general liability (CGL). As the name implies, CGL is meant to cover various unforeseen circumstances.

- Bodily Injury: Injuries to third parties that occur on your business premises or as a result of your operations.

- Property Damage: Damage to someone else's property caused by your business or employees.

- Personal & Advertising Injury: This includes claims of copyright infringement, libel, slander, or false advertising.

- Medical Payments: Covers medical expenses for injuries that occur on your property, regardless of fault.

The cost of CGL will depend on the insurance provider, the business industry, the number of employees, revenue, location, and more. My company, Piedmont Microgreens, paid $560.00 for CGL through Erie Insurance in 2024.

Our CGL will cover $1,000,000 in damages per occurrence and $2,000,000 per year, as detailed above. Who will demand to see CGL? If you're starting your microgreen business, you're likely reaching out to local, stand-alone restaurants and grocery stores, like co-ops. These customers don’t typically require proof of insurance. However, a common early stage customer that is likely to require CGL is your local farmer’s market. The Durham Farmer’s Market requires all vendors, us included, to carry CGL with certain limits. As you grow your microgreen business, CGL is a standard requirement to work with bigger buyers, such as distributors. As your business grows, you will want to pay for higher limits, and your customers could require it as well. For example, a beginning policy might cover $500,000 per occurrence and $1,000,000 aggregate. As you grow, you’ll want to pay more to double those numbers. This is a conversation you’ll have with your customers and insurance provider. In short, CGL is the only insurance you'll need for the first 6-18 months of business. This is true if you have no employees and use a personal vehicle for deliveries and farmers' markets. If someone wants to see your insurance details, they'll likely ask for a certificate of insurance (COI). You can request this from your insurance provider.

Commercial Auto Insurance

Whether you buy commercial auto insurance (CAI) or worker’s compensation insurance (WCI) first depends on a few factors. States have different laws on when to have WCI. Most states require WCI when you hire your first employee, even if they're part-time. North Carolina, which is where I operate, doesn’t require it until you have three employees. In the end, you’ll likely need WCI and CAI around the same time.

We bought our first company vehicle in June 2023. We paid Erie Insurance $2,391.00 in 2024 for our CAI policy. Clearly, CAI is much more costly than our CGL insurance. CAI will have a similar structure as CGL - single occurrence and aggregate limits. CAI can cover bodily injury, collisions, property damage, uninsured or underinsured motorist damages, medical bills, and more. Many policies will cover employees driving personal vehicles for work purposes, as well as rented vehicles. CAI will cover multiple employees, usually without a change in the cost/premium. Expect to pay much more for a commercial policy than a personal one, all else being equal. For example, I personally pay about $580.00 for my own auto policy.

CAI is required by many state governments, especially if the vehicle is company-owned. Employees will feel at ease knowing they’re covered by the company policy as well. Certain customers could require proof of insurance if you expect to be driving onto their property, but it’s otherwise uncommon for clients to explicitly require CAI.

Worker’s Compensation Insurance

As we mentioned, WCI is a state requirement, but each state’s laws are different. WCI covers medical expenses, lost wages, rehabilitation costs, and death benefits for work-related injuries or illnesses. The cost of WCI is typically calculated based on the employee's pay. Here’s how WCI is typically calculated.

Premium = (Payroll / $100) x Class Code Rate x Experience Modification Rate (EMR)

The premium is the cost to the employer.

Payroll is the employee’s wages.

The class code is specific to the industry or type of work, which is a function of the risk of injury.

EMR is a company’s claim history compared to the industry average.

There will be other costs and components to a WCI policy, but those are beyond the scope of this article. Let’s look at my company’s WCI policy from 2023.

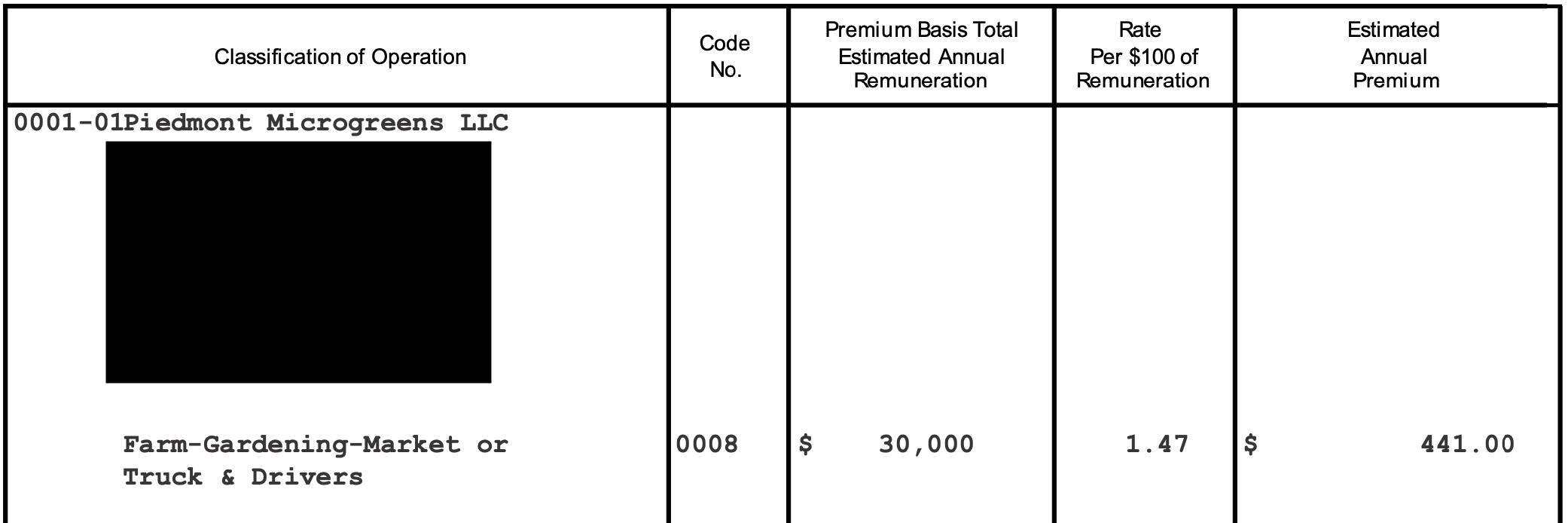

We were once insured through PIE, but now our payroll company, Paychex, handles our WCI. PIE assigned a class code of 0008 for “Farm-Gardening-Market or Truck & Drivers.” The class code insurance rate was $1.47 for every $100 of payroll. In other words, for every $100 paid out to our employees, we’d pay an additional $1.47 to our WCI. Scaling your business means more employees, which means more payroll. Higher payroll costs translates to higher WCI costs. My total payroll costs today include wages, 401k matching, taxes, payroll fees, and WCI. WCI accounts for 2% of my overall payroll costs. The nice part about WCI compared to CAI is that WCI is variable. If you downsize your business, WCI will decrease proportionally.

Conclusion

CGL, CAI, and WCI are the three main types of insurance you’ll need in the first few years of business. CAI will likely be the most expensive. CGL is relatively affordable, and WCI is variable based on payroll costs. There are other types of insurance, but they’re case specific and sometimes covered by the three aforementioned forms. Other insurance types include property insurance, business interruption insurance, cyber liability insurance, and product liability insurance.

Disclaimer

This article is NOT comprehensive. This blog is in no way financial, legal, or business advice. Do your own research before getting into business.

Share this post: